The landscape of oncology is undergoing a fundamental shift. We are moving away from a "one-size-fits-all" approach toward a future defined by precision, speed, and non-invasive detection. Cancer diagnostics—the backbone of this evolution—is no longer just about identifying a tumor; it is about characterizing the molecular blueprint of a disease to dictate exact, patient-specific treatment.

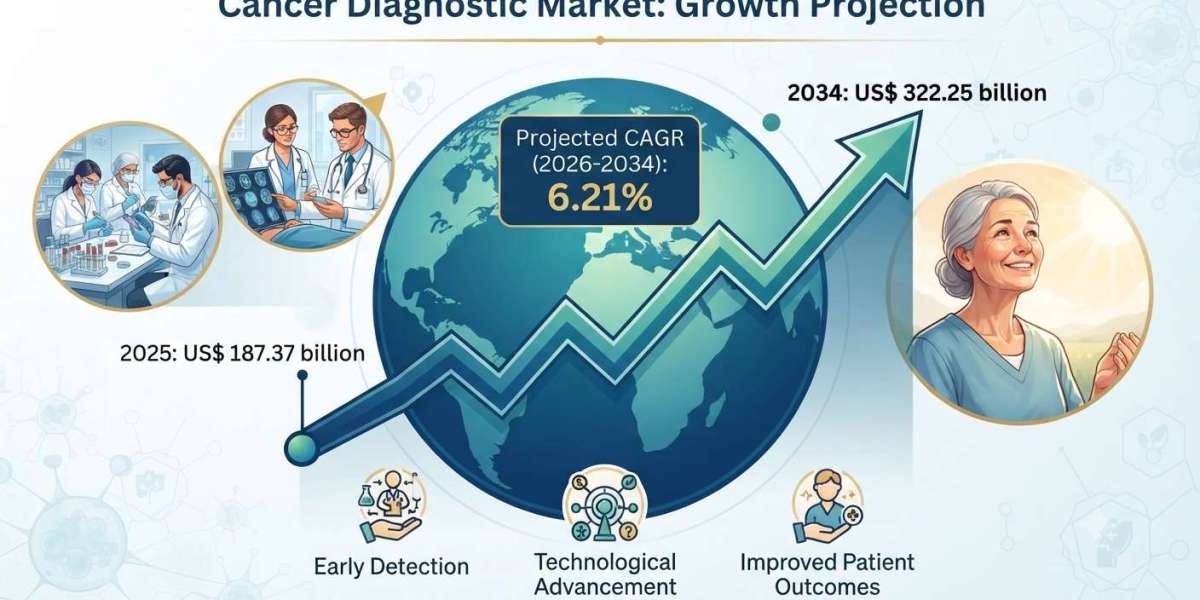

According to the latest research by Renub Research, the Cancer Diagnostic Market is expected to reach US$ 322.25 billion by 2034, growing from US$ 187.37 billion in 2025, with a steady CAGR of 6.21% from 2026 to 2034. This robust growth is powered by the rapid maturation of liquid biopsy technologies, the integration of artificial intelligence in imaging, and an ever-expanding array of companion diagnostics that link testing directly to life-saving targeted therapies.

Understanding the Cancer Diagnostic Industry

Cancer diagnostics encompasses the full spectrum of tools—from high-resolution PET scans and histopathology to advanced genomic sequencing—used to detect, confirm, and stage malignancies. By identifying specific biomarkers and genetic mutations, these diagnostic processes empower clinicians to pivot from reactive treatment to proactive, precision oncology.

Today’s diagnostic ecosystem is characterized by:

Molecular Assays: Enabling the detection of mutations at a sub-microscopic level.

Liquid Biopsies: Transforming monitoring from invasive tissue samples to simple, repeatable blood draws.

Digital Pathology and AI: Increasing the accuracy and workflow efficiency of laboratory examinations.

As healthcare systems prioritize early detection to improve survival rates, the demand for reliable, minimally invasive, and highly accurate diagnostic tools has become a global imperative.

Growth Drivers: The Engines of Precision Medicine

The rapid expansion of the market is driven by several converging factors that favor early intervention and personalized care.

1. The Rise of Liquid Biopsy and MRD Testing

Perhaps the most significant shift in modern oncology is the adoption of Minimal Residual Disease (MRD) and liquid biopsy technologies. These tests, which detect circulating tumor DNA (ctDNA) in the blood, allow clinicians to monitor patients for relapse risks long before a tumor would show up on a traditional CT scan. Recent strategic moves, such as the acquisition of Haystack Oncology by Quest Diagnostics, highlight the massive industry focus on this space. These tests offer a patient-friendly, highly sensitive alternative to surgical biopsies, revolutionizing post-treatment monitoring.

2. Companion Diagnostics and Strategic Alliances

The success of modern oncology drugs is increasingly tied to the diagnostic tools used to identify the right patients. Collaborations between diagnostic giants (like QIAGEN) and pharmaceutical firms (like Servier) have become essential. By developing companion diagnostics that identify specific gene mutations, companies ensure that patients receive the targeted therapies most likely to work for them. This symbiotic relationship between "test" and "therapy" is a primary engine for both market growth and clinical success.

3. Personalized Healthcare Ecosystems

Major collaborations—such as those between Roche and Janssen—are accelerating the discovery of new biomarkers. As treatments become more tailored, the requirement for comprehensive genomic data grows. This has led to a surge in demand for sequencing platforms and integrated digital pathology solutions, ensuring that every oncologist has access to the precision data necessary for informed decision-making.

Challenges: Bridging the Accessibility Gap

Despite the technological leap, the market faces significant headwinds:

Cost and Equity: High-end genomic sequencing and advanced imaging carry significant price tags. This creates an "access divide" where high-tech diagnostics are readily available in top-tier urban centers but remain inaccessible in lower-income regions.

Regulatory Complexity: Because these diagnostic tools influence critical medical decisions, they are subject to intense scrutiny. Navigating diverse global regulatory frameworks for validation, accuracy, and safety is a time-consuming and expensive process that can delay the rollout of innovative life-saving tests.

Regional Market Analysis

United States: As a global innovation hub, the U.S. benefits from an unmatched clinical trial ecosystem and robust reimbursement policies. The rapid integration of AI-powered imaging and NGS makes it the leader in diagnostic adoption.

Germany: Known for its rigorous standards and world-class healthcare, Germany leads Europe in the adoption of molecular diagnostics. Its focus on early screening and high-accuracy tools ensures that patients receive the most reliable diagnostic data available.

China: Driven by government-backed modernization and rising awareness, China is arguably the fastest-growing market. Significant investments in local labs and biotech capabilities are making precision oncology increasingly accessible to a massive patient population.

Saudi Arabia: Under the Vision 2030 initiative, the Kingdom is rapidly upgrading its healthcare infrastructure. By prioritizing state-of-the-art diagnostic labs and screening programs, Saudi Arabia is positioning itself as a leader in regional cancer care.

Market Segmentation at a Glance

| Category | Segments |

| Application | Breast, Colorectal, Lung, Prostate, Blood, Skin, and others |

| Test Type | Tumor Biomarkers, Imaging, Biopsy, Liquid Biopsy, Immunohistochemistry |

| End-User | Diagnostic Centers, Hospitals & Clinics, Research Institutes |

Key Industry Players

The market competitive landscape is driven by companies that bridge the gap between bench research and bedside care. Key players include:

Genomics & Molecular: Illumina, Thermo Fisher Scientific, QIAGEN N.V.

Diagnostics & Systems: Roche Holding AG, Abbott Laboratories, bioMérieux.

Imaging & Technology: Koninklijke Philips N.V.

Pharmaceuticals with Diagnostic Ties: Pfizer, Inc.

These players are consistently evaluated through their R&D investments, M&A activity, and the clinical performance of their diagnostic platforms.

Frequently Asked Questions (FAQs) - Renub Research Insights

1. What is the projected market size for Cancer Diagnostics by 2034?

According to Renub Research, the market is expected to reach US$ 322.25 billion by 2034.

2. What is the expected CAGR for the cancer diagnostic market?

The market is anticipated to grow at a CAGR of 6.21% from 2026 to 2034.

3. What are the key drivers of this market growth?

Growth is primarily driven by the rising prevalence of cancer, the adoption of liquid biopsy and MRD testing, the expansion of companion diagnostics, and increased global focus on personalized healthcare.

4. Why is "Liquid Biopsy" considered a game-changer?

Liquid biopsies offer a non-invasive, blood-based method for detecting residual disease and relapse risks, providing patient comfort and earlier intervention compared to traditional surgical biopsies.

5. How do companion diagnostics impact treatment?

Companion diagnostics ensure that targeted therapies are prescribed only to patients who possess the specific genetic mutations that the drug is designed to treat, significantly improving clinical outcomes.

6. What are the main challenges to market expansion?

The primary challenges include the high cost of advanced diagnostic technologies, unequal global accessibility, and the lengthy, complex regulatory pathways required for product validation.

7. Which regions are currently showing the highest growth potential?

While the U.S. and Europe lead in innovation, China and Saudi Arabia are experiencing rapid growth due to significant government investment in diagnostic infrastructure and healthcare modernization.

This summary provides a high-level overview of the cancer diagnostics market. For a comprehensive analysis of revenue streams, specific regional data, and in-depth company SWOT analyses, please refer to the full market intelligence report provided by Renub Research.