1) Market Overview

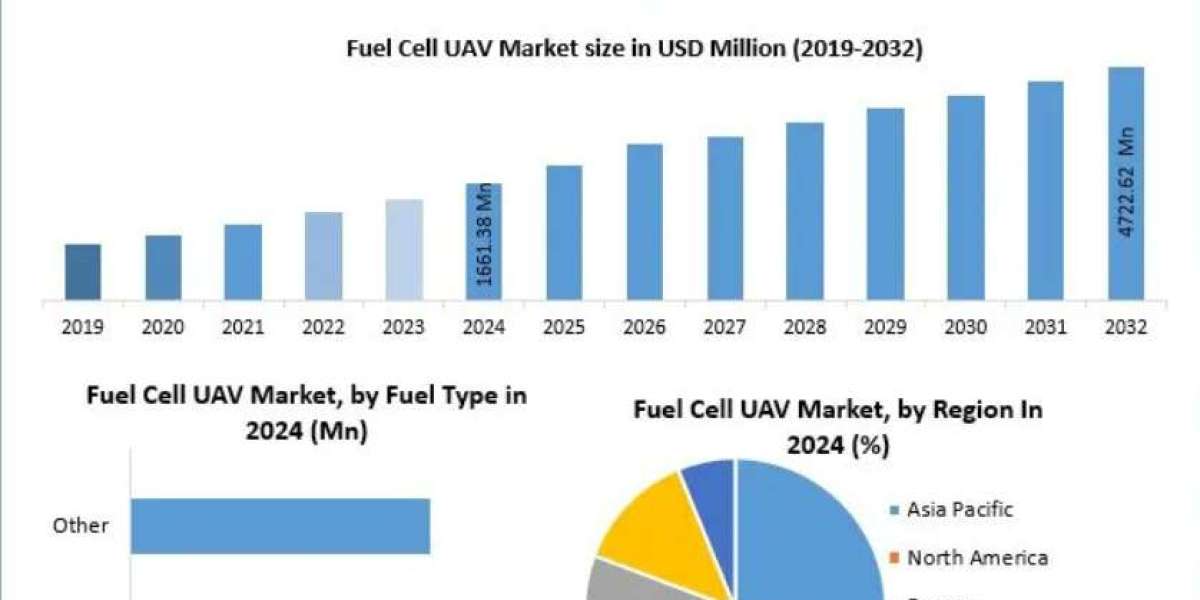

The global fuel cell unmanned aerial vehicle (UAV) market, registered a valuation of USD 1,661.38 million in 2024 and is forecast to nearly triple over the following eight years, reaching USD 4,722.62 million by 2032 at a CAGR of 13.95%. Unlike conventional battery-powered drones that plateau after 30–45 minutes of flight, fuel cell UAVs—particularly those harnessing hydrogen electrochemistry—routinely achieve multi-hour endurance, dramatically expanding the operational envelope for tasks such as wide-area agricultural mapping, pipeline corridor inspection, coastline patrol, and humanitarian logistics in geographically isolated communities.

The technology's defining characteristic is its electrochemical conversion process: hydrogen and oxygen react within the fuel cell stack to generate electricity, with water vapour as the sole exhaust product. This zero-emission profile aligns seamlessly with international commitments under the Paris Agreement and national net-zero roadmaps, positioning fuel cell UAVs as preferred procurement targets wherever environmental accountability is a procurement criterion.

Access the Future of Market Strategy: [Download the Exclusive Sample Collection Kits Handbook & Data Summary Here] https://www.maximizemarketresearch.com/request-sample/189143/

2) Market Dynamics

Driving Forces

Three convergent forces are accelerating market expansion. First, governments are committing unprecedented capital to clean hydrogen production and distribution infrastructure—most notably the U.S. National Clean Hydrogen Strategy and analogous EU hydrogen economy blueprints—lowering the total cost of ownership for hydrogen UAV operators over time. Second, the defence sector is investing heavily in persistent-ISR (Intelligence, Surveillance, and Reconnaissance) platforms; fuel cell UAVs meet the military's operational requirements for low acoustic signatures, extended loiter, and reduced logistical burden relative to fossil-fuel aircraft. Third, commercial sectors are discovering that hydrogen drones deliver 2–4 times the coverage of battery alternatives per sortie, rewriting the unit economics of large-area tasks in agriculture, utilities, and infrastructure.

Headwinds and Constraints

Despite strong momentum, the market navigates several friction points. The capital cost of procuring and certifying fuel cell systems remains a barrier for small and mid-size commercial operators. Hydrogen's storage density disadvantage—requiring either high-pressure cylinders or cryogenic containment—adds structural complexity. The absence of universally accessible refuelling infrastructure outside major urban or military corridors limits operational range. Regulatory frameworks governing hydrogen handling in airspace are still maturing across multiple jurisdictions, introducing compliance unpredictability.

3) Market Segmentation Insight

By Fuel Type

Hydrogen commands over 90% of the fuel-type segment—valued at USD 1,372.12 million in 2024—by virtue of its unmatched gravimetric energy density. Each kilogram of hydrogen stores roughly 33 kWh of usable energy, enabling UAVs to fly longer and carry more without weight penalties that would otherwise compromise mission capability. Alternative fuel cell chemistries, including direct methanol and formic acid variants, occupy a niche share and are being explored for scenarios where hydrogen logistics are impractical, such as marine-based operations or remote mining sites.

By Product Type

Proton Exchange Membrane Fuel Cells (PEMFCs) dominate at approximately 80% share. Their polymer electrolyte membranes operate at relatively low temperatures (60–80°C), enabling rapid cold-start capability—critical when drones must be scrambled quickly for emergency response or time-sensitive surveillance. Solid Oxide Fuel Cells (SOFCs), while achieving higher thermodynamic efficiency, require elevated operating temperatures and longer warm-up cycles, restricting their applicability to pre-planned, long-duration missions. Emerging hybrid and regenerative fuel cell configurations are generating R&D interest as researchers seek to combine the efficiency of SOFCs with the responsiveness of PEMFCs.

By UAV Type

Fixed-wing platforms leverage aerodynamic lift to maximise fuel cell efficiency over long distances, making them the preferred choice for border surveillance, topographic mapping, and offshore infrastructure inspection. Multi-rotor and rotary-wing UAVs sacrifice range for vertical agility, excelling in confined urban environments, search-and-rescue operations, and precision agricultural spraying. Hybrid VTOL (Vertical Take-Off and Landing) configurations are rapidly gaining commercial traction, offering the versatility of rotary take-off with the endurance of fixed-wing cruise—an increasingly attractive proposition for logistics providers navigating dense urban last-mile delivery challenges.

By Weight

Sub-50 kg UAVs led the 2024 market at USD 1,122.92 million. Their regulatory treatment under most national aviation authorities is more permissive, procurement costs are lower, and operational flexibility is higher, enabling rapid deployment across diverse mission profiles. The above-50 kg heavy-lift segment, while currently smaller, is growing faster as manufacturers scale fuel cell stack power output to support enterprise payloads—including multi-sensor surveillance suites, heavy cargo pods, and communications relay equipment—required by defence and industrial operators.

By End-User

Civil and Commercial applications captured the largest share at 35.80% (USD 520.24 million in 2024), spanning precision agriculture, aerial photography, utility inspection, and environmental monitoring. The Military & Defence segment is the second largest and arguably the most technologically demanding consumer, with requirements for extended loiter, stealth operation, and harsh-environment reliability driving cutting-edge fuel cell R&D. Logistics & Transportation is the fastest-expanding end-user category as fuel cell drones begin to prove the economics of last-mile delivery to underserved geographies. Construction & Mining operators are deploying UAVs for volumetric surveys, structural inspection, and hazardous-area monitoring, where human entry carries unacceptable risk.

4) Market Regional Insight

North America leads globally, underpinned by the world's highest per-capita defence UAV expenditure, an advanced hydrogen policy framework, and the presence of pioneering technology developers. U.S. federal investment in hydrogen hubs and clean energy R&D partnerships—exemplified by the National Renewable Energy Laboratory-Honeywell Aerospace collaboration on cartridge-based hydrogen storage—continues to yield commercialisable breakthroughs.

Europe follows closely, energised by the EU's Green Deal and a well-structured EASA regulatory pathway that reduces certification risk for fuel cell UAV manufacturers. Germany, France, and the Netherlands host significant research centres and commercial development programs. The Asia Pacific region is projected to post the highest CAGR through 2032; China's vertically integrated drone supply chain, Japan's hydrogen society initiative, South Korea's fuel cell manufacturing prowess, and India's liberalised UAV policy collectively create a formidable growth engine. Middle East & Africa and South America are emerging demand pools, where energy infrastructure expansion, agricultural modernisation, and border security are catalysing first-wave adoption.

5) Key Players

1. Adelan

2. Doosan Mobility Innovation

3. Edge Autonomy

4. Heven Drones

5. HyFly

6. Hylium Industries, Inc.

7. HYPOWER LAB Co.,Ltd

8. ISS Aerospace

9. Royal Nlr – Netherlands Aerospace Centre

10. Shanghai Pearl Hydrogen Energy Technology Co.

11. Spectronik

12. Stratospheric Platforms Ltd

13. Advent Technologies

14. AeroVironment Inc

15. Ballard Power System

16. H3 dynamics

17. Honeywell International Inc

18. Intelligent Energy limited

19. Plug power Inc.

20. Textron inc.

21. Barnard Microsystems Ltd

22. Horizon Fuel Cell Technologies

These companies are focusing on innovation, strategic partnerships, and advanced hydrogen solutions to enhance UAV performance and expand market reach.

6) FAQ

Q1. What is the projected market value of the Fuel Cell UAV industry by 2032? The market is projected to reach approximately USD 4,722.62 million by 2032, expanding from USD 1,661.38 million recorded in 2024.

Q2. Why do hydrogen fuel cells outperform batteries in UAV applications? Hydrogen offers gravimetric energy density nearly 100 times greater than lithium-ion batteries, translating into flight endurance of 2–5 hours versus 30–45 minutes for comparable battery-powered platforms.

Q3. Which end-user segment is growing fastest? Logistics and Transportation is the fastest-growing end-user segment, driven by the commercial viability of hydrogen drones for last-mile and remote-area delivery.

Q4. How does regulation affect fuel cell UAV deployment? Regulatory bodies such as the FAA and EASA are actively developing updated frameworks for hydrogen UAV certification. While evolving regulations introduce short-term compliance uncertainty, they are ultimately expected to create structured pathways that facilitate broader commercial deployment.

Q5. What weight class dominates the market? UAVs weighing less than 50 kg dominate current revenues due to lower procurement costs, easier regulatory compliance, and broad commercial applicability across inspection, agriculture, and delivery missions.

Q6. What fuel cell type is most commonly used in UAVs? Proton Exchange Membrane Fuel Cells (PEMFCs) account for approximately 80% of product-type market share, valued for rapid cold-start capability, high power-to-weight ratio, and proven operational reliability.

Q7. Which region leads the Fuel Cell UAV market? North America held the leading regional position in 2024, with the Asia Pacific region expected to record the highest CAGR through the forecast period.

Elevate Your Competitive Intelligence: > [Click to Access the Complete Sample Collection Kits Strategy Handbook and Data Summary] https://www.maximizemarketresearch.com/request-sample/189143/

7) About Maximize Market Research

Maximize Market Research Pvt. Ltd. is a Pune-headquartered global market intelligence and consulting firm serving clients across 40+ countries. The company delivers rigorously researched reports, competitive benchmarking, and strategic consulting across verticals including Aerospace & Defence, Healthcare, Information Technology, Energy & Power, and Industrial Manufacturing. MMR's analytical methodology integrates primary interviews with industry practitioners, secondary data validation, bottom-up and top-down market modelling, and scenario-based forecasting to equip decision-makers with intelligence they can act on.

Contact Maximize Market Research:

3rd Floor, Navale IT Park, Phase 2

Pune Bangalore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656